If you’re a software-as-a-service (SaaS) company, you no doubt are incurring a significant amount of costs to develop software. If you’re a startup in this industry and you’ve raised your Seed round and are hoping to raise a Series A round, and you’re scrappy with an intense focus on developing or improving your core product then I am confident capitalization of software development costs is one of the last things on your mind, and if you have an in-house accountant or controller it’s probably way down on their list as they are just trying keep up with the pace of change and implement the blocking and tackling processes necessary to have a high functioning finance team.

In this article we will explore how software development costs should be treated for SaaS companies and why it may be something you want your finance team to begin addressing.

THE LEGACY MODEL

Under the legacy model of selling software where enterprise software companies sold “on-premises” software solutions and the customer took ownership of the license and installed the software on their own servers it was very clear that you followed the software capitalization rules in ASC 985, Software, which is followed for software costs when the entity intends to sell or lease the software. This standard had a high bar for when you could capitalize software development costs. You had to demonstrate you had reached “technological feasibility,” which is defined as follows:

“For purposes of this Subtopic, the technological feasibility of a computer software product is established when the entity has completed all planning, designing, coding, and testing activities that are necessary to establish that the product can be produced to meet its design specifications including functions, features, and technical performance requirements.”

– ASC 985-20-25-2

Once you achieved technological feasibility you begin to capitalize your software development costs up to the point that you release the software to customers. Upon release you begin to amortize those capitalized costs over the expected life of the software product.

Due to this high bar, many software companies essentially defaulted to asserting that the point at which technological feasibility was reached was so close to when the product was released to their customers that any amount of costs that should have been capitalized were not material. The underlying beauty of this policy (assuming it was representative of actual circumstances) is that it allowed software companies to forgo the hassle of implementing detailed time tracking systems for their developers to use in order to understand, at least materially, what costs should be capitalized. In all of my travels working with software companies I have yet to meet a developer that gets excited about time tracking, even when it can result in qualifying for an R&D tax credit, which is a topic for another time.

ENTER THE SAAS MODEL

Fast forward from the 1980s, 1990s, and early 2000s and today advancements in internet infrastructure allow people to access data intensive applications via the web.

So, you may be asking yourself…how is software development costs any different in a SaaS model versus the legacy model? Frankly, it is not different. What’s different is the accounting. And this is where much confusion and divergence in practice have occurred for several years.

Under current accounting guidance if you don’t fall into the scope of ASC 985, which for simplicity sake is the legacy “on-premise” model for selling software, then what guidance do you fall under? The only other guidance that governs costs to develop software is ASC 350-40, Accounting for Costs of Internal-Use Software. The scope of ASC 350-40 states,

“Subtopic 350-40 applies to the accounting for internal-use software. Internal-use software is software that has both of the following characteristics:

• The software is acquired, internally developed or modified solely to meet the entity’s internal needs, and

• During the software’s development or modification, no substantive plan exists or is being developed to market the software externally.

Software that is to be sold, leased or otherwise marketed is to be accounted for in accordance with Topic 985, Software.”

Are you confused yet?

A literal reading of the scope of ASC 350-40 would clearly seem to indicate that this accounting guidance would not apply to a SaaS company because the only reason you are developing software is for the purpose of marketing the software externally. And if you’re telling me a SaaS company does not meet the scope of ASC 985 and on the surface does not appear to meet the scope of ASC 350 then what guidance do we follow? This is where all of the interpretations have come to the conclusion, including Big 4 interpretations, that SaaS companies are to follow ASC 350 when determining which costs to capitalize for software development. The reason for this interpretation is that SaaS companies are in fact not actually selling software but are selling access to the software via a subscription and hosting arrangement. The general conclusion is that essentially, you’ve built internal-use software that you are now selling access to.

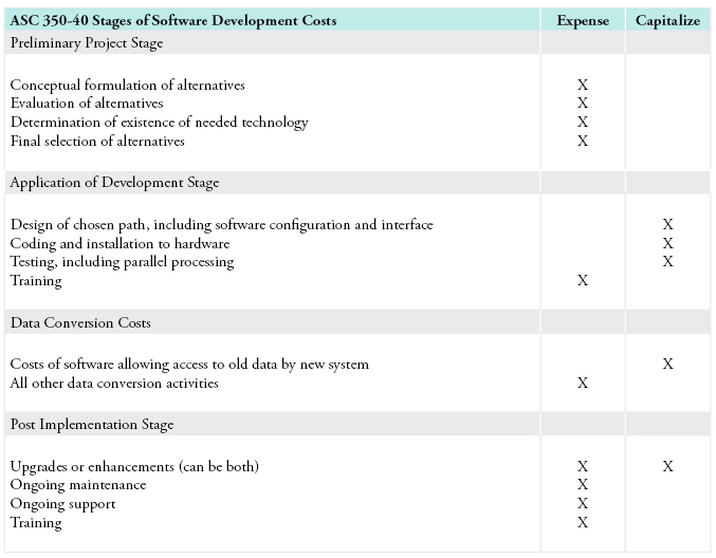

ASC 350 also has a much lower bar for when you start capitalizing your software development costs. You begin capitalizing software development costs after you exit the preliminary project stage and enter the application development stage. You cease capitalization when you enter the post-implementation stage and begin amortizing the costs at that point over the expected software product life.

Examples of the types of costs that should be expensed or capitalized include:

INDUSTRY PRACTICE AND EVOLUTION

A study published in 2016 by a regional CPA firm found that 61% of 89 public SaaS companies capitalized software development costs. This study can be misleading on the surface because if you have “on-premise” and SaaS selling models then you would follow the stricter ASC 985 guidance for all of your software development, which often times will result in little to no capitalization. This is evidenced by reviewing the 2016 10-K of Adobe, Inc. where they state they expense costs that fall into the scope of ASC 985 and capitalize costs that are for internal-use software. Presumably, the internal-use software at Adobe is truly internal-use and not part of their suite of SaaS products offered under a subscription.

Adobe 2016 10-K Disclosure

Software Development Costs – Capitalization of software development costs for software to be sold, leased, or otherwise marketed begins upon the establishment of technological feasibility, which is generally the completion of a working pro-totype that has been certified as having no critical bugs and is a release candidate. Amortization begins once the software is ready for its intended use, generally based on the pattern in which the economic benefits will be consumed. To date, soft-ware development costs incurred between completion of a working prototype and general availability of the related product have not been material.

Internal Use Software – We capitalize costs associated with customized internal-use software systems that have reached the application development stage. Such capitalized costs include external direct costs utilized in develop-ing or obtaining the applications and payroll and payroll-related expenses for employees, who are directly associated with the development of the applications. Capitalization of such costs begins when the preliminary project stage is complete and ceases at the point in which the project is substantially complete and is ready for its intended purpose.

It should be noted that this disclosure does not appear in Adobe’s most recent 10-K and may be due to the evolution of their business to an almost exclusive SaaS model.

Another disclosure worth reviewing is that of Hubspot as they are a pure SaaS company with no “on-premise” sales.

Hubspot 2018 10-K Disclosure

Software development costs consist of certain payroll and stock compensation costs incurred to develop functionality for our Growth Platform and internally built software platforms, as well as certain upgrades and enhancements that are expected to result in enhanced functionality. We capitalize certain software development costs for new offerings as well as upgrades to our existing software platforms. We amortize these development costs over the estimated useful life of two to five years on a straight-line basis. We believe there are two key estimates within the capitalized software balance, which are the determina-tion of the useful life of the software and the determination of the amounts to be capitalized.

We determined that a two to five-year life is appropriate for our internal-use software based on our best estimate of the useful life of the internally developed software after considering factors such as continuous developments in the technology, obsolescence and anticipated life of the service offering before significant upgrades. Based on our prior experience, inter-nally generated software will generally remain in use for a minimum of two to five years before being significantly replaced or modified to keep up with evolving customer and company needs. While we do not anticipate any significant changes to this two to five-year estimate, a change in this estimate could produce a material impact on our financial statements. For ex-ample, if we received information that indicated the useful life of all internally developed software was one year rather than two, our capitalized software balance would decrease by approximately 50% and our amortization expense would increase by 50% in the year of adoption of the change in estimate.

These diclosures provide additional clarity that a pure SaaS company will fall under the scope of ASC 350-40 when deter-mining when and what types of costs should be capitalized for software development.

THE BOTTOM LINE

The practice of capitalizing software development costs in the SaaS industry has started to become the norm with many publicly traded SaaS companies following the guidance in ASC 350-40. This is an area where SaaS companies will want to start to take a harder look at and determine which, if any, of their software development costs should be capitalized since the industry is moving in that direction.

For additional assistance or if you have questions contact:

Klint Lewis, Audit Partner, Technology Practice, Tanner LLC

801-924-5103 | klewis@tannerco.com