Employee Benefit Plans: Top 10 Most Common Plan Errors

Posted by Kathryn Fargam in Assurance, Blog, on

Employee Benefit Plans: Top 10 Most Common Plan Errors

Errors within employee benefit plans are more common than you may think. As a plan sponsor, you have a responsibility to ensure your company’s plan is being operated in accordance with the Internal Revenue Code (IRC) and ERISA regulations. Despite a company’s best effort, errors do occur.

In this article, we will explore the top 10 most common plan errors and offer a solution on how to avoid or correct them.

1. PARTICIPATION/ELIGIBILITY

The first common error relates to the admission of participants into the plan. This typically occurs via not offering eligible participants the opportunity to participate in the plan, or there is a failure to admit employees into the plan on a timely basis.

Employers occasionally assume the plan doesn’t cover certain employees, such as part-time employees. The plan document should include a definition of “employee” and provide requirements of when an employee becomes eligible to participate in the plan. The IRC allows an employer to impose an eligibility waiting period of up to one year of service (and 1,000 hours) before employees can commence participation in a qualified retirement plan. A plan cannot require an employee to be older than 21 to participate.

The failure to accurately determine employee eligibility for a 401(k) plan can jeopardize the plan’s tax qualification status. Additionally, an error involving eligibility is a violation of ERISA as well.

Solution: Each employee who receives a Form W-2 should be included in the retirement plan as an eligible employee, unless you can properly exclude that employee by the plan terms. Determine each employee’s eligibility using the plan definition of eligible employee, via the plan age and service requirements. Closely monitor employees’ attainment of the plan’s eligibility criteria and timely provide eligibility information to plan service providers. Add a procedure to the new hire orientation where all individuals are provided information about the plan and when they become eligible to participate in the plan. Maintain documentation evidencing that all eligible employees were given the opportunity to participate in the plan. If an employee was accidentally excluded, use the IRS approved correction method under the Employee Plans Compliance Resolutions System (EPCRS.)

2. COMPENSATION

The second common error is due to an incorrect definition of compensation being used to calculate contributions. It is common that employers erroneously exclude certain types of compensations (e.g. severance pay, bonuses, forms of equity compensation) when calculating contributions including the employer match. IRC limits on contributions and compensation should also be monitored.

Plan participants are entitled to make and receive contributions based on the definition of “compensation” that is laid out in the plan documents. Failing to comply with the language laid out in the plan document could mean that the plan becomes disqualified.

There are two annual limits that apply to contributions. First, a limit on employee elective salary deferrals. Second, an overall limit on contributions to a participant’s account. The limit applies to the total of:

■ Elective deferrals (but not catch-up contributions)

■ Employer matching contributions

■ Employer nonelective contributions

■ Allocations of forfeitures

The limit on employee elective deferrals (for traditional and safe harbor plans) is $19,500 in 2020 and was $19,000 in 2019. If permitted by the 401(k) plan, participants age 50 or over at the end of the calendar year can also make catch-up contributions. For the catch-up contributions you may contribute additional elective salary deferrals of $6,500 in 2020 and $6,000 in 2019 to traditional and safe harbor 401(k) plans.

Annual contributions to all of a participant’s accounts maintained by one employer (and any related employer)—this includes elective deferrals, employee contributions, employer matching and discretionary contributions, and allocations of forfeitures to the participant’s accounts, but not including catch-up contributions—may not exceed the lesser of 100% of the participant’s compensation or $57,000 for 2020 ($56,000 for 2019). This limit increases to $63,500 for 2020 ($62,000 for 2019) if you include catch-up contributions. In addition, the amount of compensation that can be taken into account when determining employer and employee contributions is limited to $285,000 in 2020 ($280,000 in 2019).

Solution: Check with the plan administrators to make sure that compensation is being computed correctly. To avoid plan disqualification, follow EPCRS correction principles which will most likely resulting in making extra profit-sharing contributions, plus lost earnings to make the employees whole.

Excess deferrals should be distributed back to the plan participant before April 15th following the plan year end. If the excess deferral is not distributed to the participant before April 15th, the excess deferral left in the plan is taxed twice. Also, if the entire deferral is allowed to stay in the plan, the plan may not be a qualified plan.

3. VESTING

The next common error is due to incorrect vesting being calculated due to re‐hires and incorrect vesting being calculated based upon a year of service being awarded when 1,000 hours are worked.

An employee’s rights to retirement benefits are determined through the application of a vesting schedule. A vesting schedule defines vesting in terms of percentages, which are in turn determined based on the employee’s number of years of service. Rehired employees who had previously completed the plan’s eligibility requirements before terminating, may begin participating immediately upon rehire. However, if the employee’s original entry date would have been later, then the later entry date applies. Not properly accounting for an employee’s rehire and eligibility date will result in incorrect vesting being calculated for that employee.

A 401(k) plan may not require more than a year of service as a condition of being eligible to participate in the plan. A year of service means a calendar year, plan year, or any other consecutive 12-month period during which the employee completes at least 1,000 hours of service starting on the employment commencement date. Plan administrators need to be mindful to consider this in determining the vesting schedule of the plan participant.

If a defined contribution plan fails to apply the proper vesting percentage to an employee’s account balance, it may result in a in forfeiture of too much of the employee’s account balance.

Solution: Calculating the vesting percentage of enrolled participants accurately and timely is vital for employers maintaining defined contribution plans. The plan document, employee data, etc., should be carefully reviewed to ensure that employees are correctly credited with vesting service. When a participant is receiving a benefit pay out, a quick check of the employee’s vesting percentage can prevent these errors before they occur. Remember to pay special attention to re-hires and first year participants in calculating the vesting schedule for plan participants. Vesting schedule errors may be corrected under EPCRS.

4. HARDSHIP DISTRIBUTIONS

The Bipartisan Budget Act of 2018 enacted three changes to the rules over hardship distributions, specifically:

■ Repealing the previously required 6-month suspension of elective deferrals after a participant received a hardship distribution;

■ Permitting amounts previously contributed as qualified non-elective or qualified matching contributions (QNECs/QMACs) to be available as a hardship distribution; and

■ Removing the requirement to take available plan loans prior to requesting a hardship.

Solution: Although the Act is effective for hardship distributions made in 2019, taxpayers can rely on these rules for purposes of hardship distributions made in 2018 as well. Plan management should be familiar with these changes and make plan participants aware of the changes.

5. LOANS

Another common error is failing to report loan defaults.

Loans that exceed the maximum amount or don’t follow the required repayment schedule are considered “deemed distributions.” If the loan repayments are not made at least quarterly, the remaining balance is treated as a distribution that is subject to income tax and may be subject to the 10% early distribution tax. If the employee continues to participate in the plan after the deemed distribution occurs, he or she is still required to make loan repayments. These amounts are treated as basis and will not be taxable when later distributed by the plan. A loan that goes into default is a deemed distribution of the entire unpaid loan balance plus accrued interest.

Solution: If participant loans under your plan do not meet the legal requirements, or if repayments have not been made according to the schedule set out in the loan document, you may be able to correct these problems using the Voluntary Correction Program (VCP). Employers need to have a system in place to ensure that plan loans are administered in compliance with the plan document and any separate written loan policy that has been adopted. Employers should work with plan administrators to ensure that administrators have participant loan information to verify that the proper loan payments are being timely made.

6. TIMELINESS

The failure to consistently remit participant contributions in a timely manner is another common error employers tend to make.

The employer is responsible for contributing the participants’ deferrals to the plan trust. Sometimes employers wait too long to remit participant contributions into the plan. The general rule for deposits of 401(k) withholdings requires that the plan sponsor remit withheld employee deferrals to the plan as soon as administratively feasible. However, these deposits cannot be made later than 15 business days after the end of the month in which the contributions are withheld. There is no “safe harbor” with respect to this timeline. Investigations and audits by the DOL have demonstrated that the DOL reviews the history of a plan sponsor’s deposits, takes the earliest deposit during that time, and then applies that as the standard of timeliness that all deposits should meet. The DOL has published its views that electronic transfers of funds allow remittances to be made in very short periods of time. The DOL has further ruled that a plan sponsor should pay lost earnings on any untimely remitted funds.

Solution: Establish a procedure requiring elective deferrals to be deposited coincident with or after each payroll per the plan document. If deferral deposits are late because of vacations or other disruptions, keep a record of why those deposits were late. Implement practices and standard operating procedures to ensure that employees know when deposits must be made.

Correction through EPCRS may be required if the terms of the plan weren’t followed. Correction for late deposits may require you to:

■ Determine which deposits were late and calculate the lost earnings necessary to correct to the late remittance.

■ Deposit any missed elective deferrals, together with lost earnings, into the trust.

■ Review procedures and correct deficiencies that led to the late deposits.

7. OVERSIGHT

The next error we will cover is due to failure of the plan oversight committee to meet regularly and properly discharge its fiduciary responsibilities. Keep in mind this also includes failure of the plan oversight committee to keep minutes of meetings held.

Many of the actions needed to operate a 401(k) plan involve fiduciary decision—whether you hire someone to manage the plan for you or do some or all the plan management internally. Controlling the assets of the plan or using discretion in administering and managing the plan makes you or the entity you hire a plan fiduciary to the extent of that discretion or control. Thus, fiduciary status is based on the functions performed for the plan, not a title. Be aware that hiring someone to perform fiduciary functions is itself a fiduciary act.

Solution: The plan oversight committee should meet regularly to evaluate the plan, to review the documents for law changes, update them as necessary, and to properly discharge all of its fiduciary responsibilities. These plan oversight committee meetings should be properly memorialized with meeting minutes.

8. DOCUMENTATION

This next common error is a failure to document participants’ requested changes to deferral amounts.

As an employer sponsoring a retirement plan, you are required by law to keep your books and records available for review by the IRS and/or Department of Labor. Having these records will also facilitate answering questions when determining participants’ benefits and when the plan is being audited. Frequently, plans fail to document participants’ requested changes to deferral amounts. This can lead to incorrect withholdings and contributions into a participants account.

Solution: Keep detailed records of participants’ requested changes to deferral amounts and process the changes timely. The plan will need to follow the EPCRS correction principles to make the employees whole for missed contributions.

9. INTERNAL CONTROLS

This next error is caused by a failure to reconcile contributions per the payroll ledger to contributions received by the asset custodian, and to reconcile the census to the payroll information.

On occasion, the payroll ledger and the submission of contributions to the asset custodian do not agree to each other. This results in participant accounts not being accurately reflected. In addition, sometimes management of the plan does not perform a reconciliation between the census and payroll records at the end of the year. This could result in the census not including all employees who received compensation during the year. An employee census with incomplete or inaccurate payroll information can result in the plan being noncompliant with DOL regulations and required nondiscrimination tests.

Solution: Plan management should implement controls and procedures to ensure all contributions are accurately transmitted and recorded properly and timely as plan assets. Ongoing reconciliation with each pay period would serve to prevent prohibited transactions resulting from amounts withheld and not timely remitted to the plan.

Plan management should implement controls to ensure the census data is complete and accurate and agrees with the payroll records of the plan sponsor.

10. ADP AND ACP NONDISCRIMINATION TESTS

Our final common error covered in this article is the plan failing the 401(k) ADP and ACP nondiscrimination tests.

Plan sponsors must test traditional 401(k) plans each year to ensure that the contributions made by and for rank-and-file employees (non-highly compensated employees (NHCE)) are proportional to contributions made for owners and managers (highly compensated employees (HCE)). As the NHCEs save more for retirement, the rules allow HCEs to defer more. These nondiscrimination tests for 401(k) plans are called the Actual Deferral Percentage (ADP) and Actual Contribution Percentage (ACP) tests. Sometimes these tests fail and must be corrected.

Solution: Complete an independent review to determine if you properly classified HCEs and NHCEs, including all employees eligible to make a deferral, even if they chose not to make one. If your plan fails the ADP or ACP test, you must take the corrective action described in your plan document during the statutory correction period to rectify the errors found. To avoid this issue, consider a safe harbor plan design or using automatic enrollment. Communicate with plan administrators to ensure proper employee classification and compliance with the plan terms.

About Tanner LLC’s Employee Benefit Plan Practice

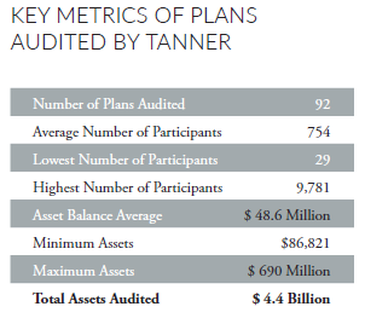

Tanner is a regional accounting firm based in Salt Lake City, Utah with clients located across the United States but with a regional concentration in the Western United States. There are 18 partners and 160 total employees. The firm’s benefit plan practice currently consists of 92 employee benefit plan clients with the following characteristics:

For further information, contact:

Klint Lewis, Audit Partner, Tanner LLC 801-924-5103 | klewis@tannerco.com

Doug Hansen, Audit Partner, Tanner LLC 801-924-5165 | djhansen@tannerco.com

Kent Van Leeuwen, Audit Director, Tanner LLC 801-924-5166 | kvanleeuwen@tannerco.com

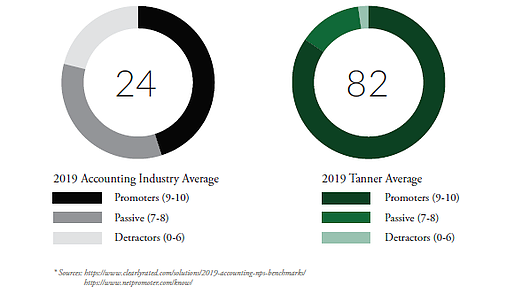

NET PROMOTER SCORE COMPARISON

Net Promoter Score (NPS) is a management tool that was developed by Bain & Company to gauge the loyalty of a firm’s customer relationships. Tanner’s NPS is second to none in the accounting industry and is a result of our focus on our clients.

For a printable version of this article, please click here.

Schedule a Call